Decreto 6-2026 Ends Inheritance Tax in Guatemala After 70 years

Decreto 6-2026 eliminates inheritance tax in Guatemala, benefiting ongoing cases and ending decades of penalties, interest, and complex procedures.

Decreto 6-2026 officially eliminates the inheritance tax in Guatemala as of April 2, 2026, ending more than 70 years of taxation and extending the benefit to cases that were already in process.

Tax repeal takes effect after publication

The repeal of the inheritance, legacy, and donation tax comes into force following the publication of Decreto 6-2026 in the Diario de Centro América on March 2, establishing its validity 30 days later.

With this change, beneficiaries are no longer required to pay taxes on inheritances, legacies, or donations due to death. The measure also applies to ongoing succession processes, including intestate, testamentary, and donation-related cases.

Immediate impact on ongoing legal processes

The new regulation mandates that administrative entities handling cases previously subject to tax liquidation must return the files to the interested parties without requiring any formal request.

“Files must be returned to beneficiaries without the need for additional procedures,” as outlined in the law.

In parallel, judges and notaries overseeing these processes must continue proceedings under current legal frameworks. Once completed, they are required to submit certifications or official records to the corresponding registries and notify relevant offices to proceed with asset transfers.

Importantly, these transfers will no longer require any tax assessment or payment related to inheritance or death-related donations.

Legal reforms linked to the repeal

Decreto 6-2026 also introduces modifications to several legal provisions.

Changes were made to Article 489 of Decree Law 107 (Civil and Commercial Procedural Code), maintaining its first paragraph while updating references from the “Ministry of Finance and Public Credit” to the “Ministry of Public Finances.”

Additionally, the requirement for notifying the Superintendence of Banks or other authorities regarding the valuation of shares or securities has been removed.

The decree also amends Article 7 of Decree 27-92 (Value Added Tax Law),

expanding exemptions to include “donations between living individuals up to the second degree of consanguinity and first degree of affinity."

Similarly, Article 8 of Decree 10-2012 (Tax Update Law) was updated to remove references to the now-repealed inheritance tax law, maintaining exemptions for inheritances, legacies, and donations due to death.

Why the inheritance tax was eliminated

The repeal responds to longstanding issues in the inheritance process, which had become highly bureaucratic and financially burdensome for beneficiaries.

Under the previous framework, the tax obligation began six months after the death of the estate owner. Delays triggered penalties of up to 100% of the tax amount, along with a 1% monthly interest charge on outstanding balances.

“Penalties and interest accumulated over time, often making it impossible for heirs to pay,” reflecting the practical challenges faced under the old system.

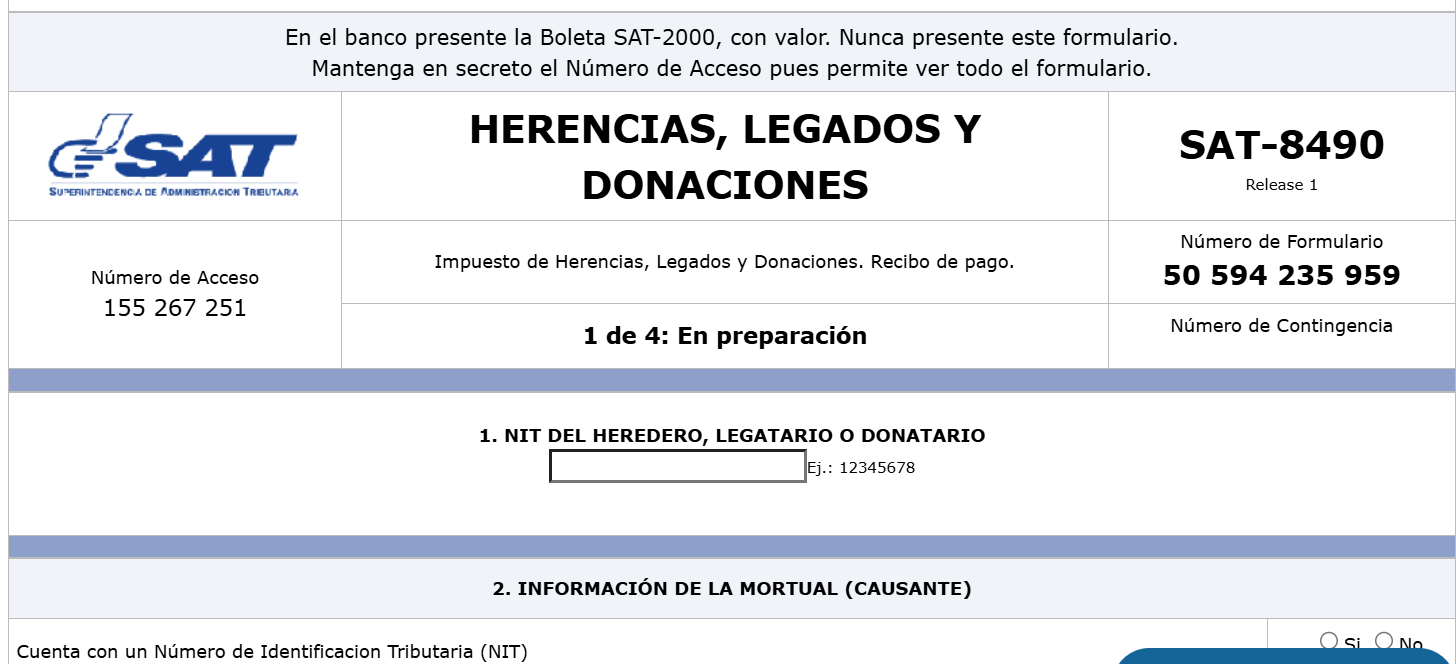

Beneficiaries were required to complete payment within 10 days using the SAT-8490 form through the Declaraguate platform.

In practice, inheritance processes often took years to complete before reaching the tax liquidation stage. As a result, fines and interest continued to grow, leading in some cases to heirs being unable to claim inherited assets.

End of a decades-long tax burden

With the elimination of the inheritance tax, Guatemala removes a financial and administrative barrier that had affected beneficiaries for decades.

The implementation of Decreto 6-2026 not only simplifies legal procedures but also prevents the accumulation of penalties that previously put inherited assets at risk.